EUSPA's 12 May 2026 Copernicus Demonstrators showcase — insurance and finance, energy, and fisheries and aquaculture. The funding-pillar anchor of the W22 European autonomy week. Space Insights.

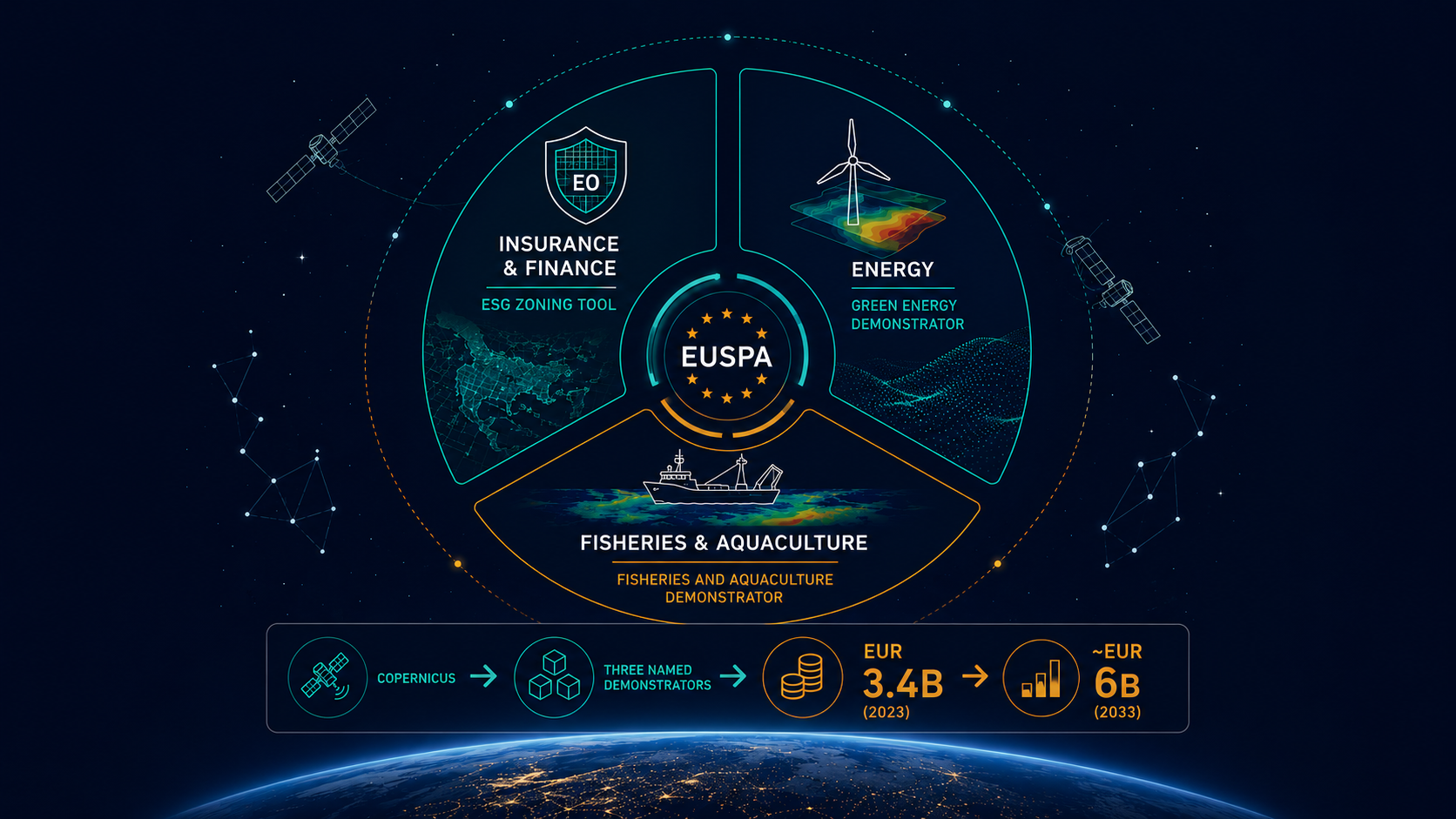

On 12 May 2026 the European Union Agency for the Space Programme (EUSPA) published a showcase of three Copernicus Demonstrators highlighting how Earth observation data is being operationalised across three downstream sectors: insurance and finance, energy, and fisheries and aquaculture. The communication frames downstream service providers as the route through which Copernicus capability translates into commercial uptake, and names three specific demonstrator projects covering the three sectors. EUSPA's communication anchors the sector framing in market size: "in 2023, global revenues from EO data and value-added services amounted to EUR 3.4 billion. By 2033, that number is set to almost double, reaching nearly EUR 6 billion in revenue."

Space Insights cross-file editorial read

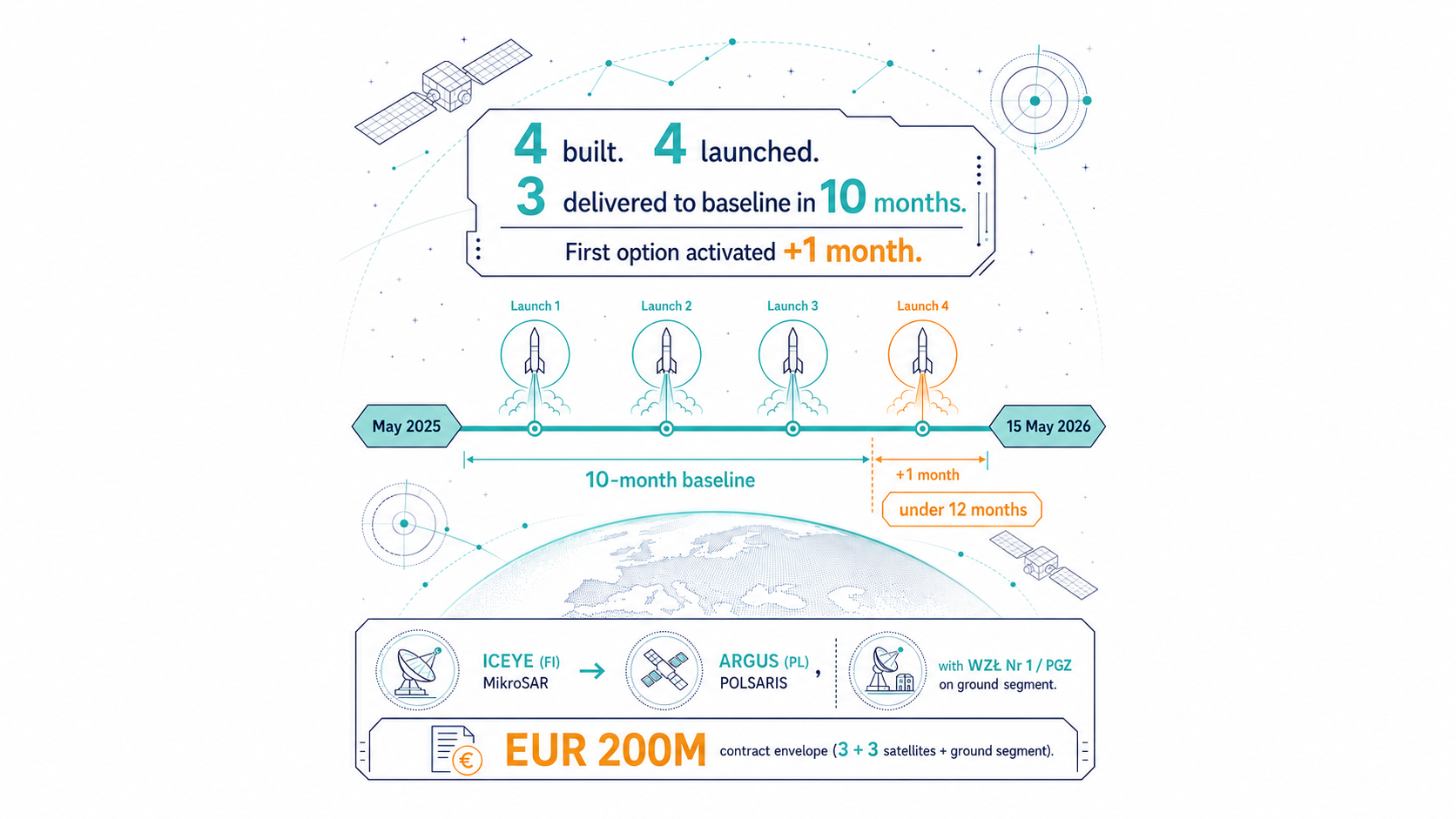

What EUSPA published, and how Space Insights reads it. EUSPA's own communication is a demonstrator showcase. Space Insights reads it as the commercial-value layer of the week's wider autonomy mix — alongside Aschbacher's 18 May op-ed (W22 Signal 3), the 19 May Helsing-OHB KIRK joint venture (W22 Signal 10), the 15 May ICEYE MikroSAR / POLSARIS handover to Poland's ARGUS agency (W22 Signal 18) and the 21 to 23 May GLOBSEC 2026 panel (W22 Signal 4). The autonomy-side signals position the institutional and prime-architecture layers; the EUSPA Demonstrators publication is a commercial-value layer that helps make the long-run autonomy thesis economically legible. This is a Space Insights editorial framing of the W22 mix, not an EUSPA statement; the primary source is the EUSPA 12 May communication, and the cross-Article references are to Space Insights' own W22 coverage of the autonomy signals.

What EUSPA published

The 12 May 2026 EUSPA news article records that the insurance and finance, energy, and fisheries and aquaculture sectors "can all benefit from using Earth Observation data". The communication positions downstream service providers as the operationalisation layer; raw Copernicus data alone does not produce commercial uptake.

EUSPA names three specific demonstrators:

- ESG Zoning tool (Insurance and Finance Demonstrator) — climate-risk and environmental-impact assessment on assets, ESG reporting for regulatory compliance, sustainability assessment for ESG-strategy companies, and risk assessment for insurance and banking, drawing on Copernicus Land Monitoring (CLMS), Climate Change (C3S) and Atmosphere Monitoring (CAMS) data. The tool was built for four Czech banks (Komerční banka, Raiffeisen Bank, Moneta Money Bank and Československá obchodní banka) and currently covers areas of the Czech Republic, with geographic expansion possible according to EUSPA's framing.

- Green Energy Demonstrator — a web-based spatial planning tool for renewable-energy infrastructure site selection and environmental assessment, integrating Copernicus CLMS, C3S, CAMS and Marine (CMEMS) data with local information.

- Fisheries and Aquaculture demonstrator — a Copernicus CMEMS and EMODnet integration for fisheries and aquaculture operations, including a seaweed-farming use case, monitoring ocean and water-quality parameters and identifying seasonal and spatial patterns.

For Programme Managers writing post-2027 EO and downstream-services strategy, the load-bearing read is the sector composition. The 12 May communication is not a full Copernicus sector map; it highlights three demonstrator sectors and does not use this article to foreground agriculture, maritime safety or security applications. The three sectors named here are commercial-revenue domains where European downstream service providers are building businesses on Copernicus data layers.

Why these three sectors

The three sectors are useful editorially because they represent commercial-uptake domains where EO data can be converted into value-added services. The 12 May EUSPA communication names the three demonstrators above; the broader sectoral use-case context below is Space Insights' synthesis of the EO industry application set, not directly attributed to the EUSPA 12 May release.

Insurance and finance. EO industry application context includes underwriting and claims processing using satellite-derived risk maps for property exposure, natural-hazard claims and crop-insurance index products, with parametric insurance products in particular aligned to sustained Copernicus time-series data. EUSPA's ESG Zoning tool sits inside this broader application set with its specific focus on climate risk, ESG reporting, sustainability and risk assessment for the Czech four-bank consortium.

Energy. EO industry application context includes yield forecasting for renewables (wind, solar), infrastructure monitoring for transmission and pipeline networks, atmospheric-composition monitoring relevant to emissions reporting, and resource-exploration screening. EUSPA's Green Energy Demonstrator targets the upstream site-selection and environmental-assessment step in renewables development specifically, drawing on the multi-service Copernicus stack (CLMS, C3S, CAMS, CMEMS). The energy vertical has been a Copernicus uptake target since the Atmosphere Monitoring Service (CAMS) and the Climate Change Service (C3S) reached operational maturity.

Fisheries and aquaculture. EO industry application context includes vessel-tracking, illegal-fishing detection, ocean-colour monitoring for chlorophyll concentration and sea-surface-temperature products for fisheries management, plus aquaculture site selection and harmful algal bloom detection. EUSPA's Fisheries and Aquaculture demonstrator extends the aquaculture-side use case through CMEMS and EMODnet, with seaweed-farming operational monitoring among the named applications.

These are sectors where private-sector willingness to pay for value-added services derived from Copernicus open data has been visible in the public market for several years. The EUSPA Demonstrators read as one institutional vehicle for that conversion; the wider Copernicus user-uptake architecture sits across multiple EUSPA and Commission programmes.

How the Demonstrators connect to EUSPA's procurement and market-development pipeline

The Copernicus Demonstrators communication arrives the same week as the closing window for EUSPA Make-it-with-Space (EUSPA-OP-07-25), a downstream-services procurement framework with a 19 May 2026 deadline (procurement-specific budget terms per the EUSPA call documentation; W20 Space Insights coverage carried the ceiling figure from the original tender publication). The two communications read as a coherent EUSPA institutional posture: the Demonstrators show what downstream-services uptake looks like in operation, and the Make-it-with-Space procurement opens the funding channel for the next wave of downstream service-provider engagement.

For European downstream-services SMEs, the practical read is that EUSPA's market-development pipeline is operating on two simultaneous tracks: the demonstration-of-outcomes track (Demonstrators) and the procurement-of-future-services track (Make-it-with-Space and successor calls). Programme Managers writing 2027 to 2030 strategy should plan against both tracks rather than against either in isolation.

The funding pillar context for W22

The W22 signal mix is dominated by policy-and-autonomy signals (Aschbacher op-ed, GLOBSEC 2026), prime-architecture announcements (KIRK joint venture) and operational-delivery cases (ICEYE MikroSAR / POLSARIS handover). The EUSPA Copernicus Demonstrators signal is the W22 funding-pillar entry and carries the most directly actionable content of the week for SMEs and downstream-services providers.

The funding-pillar weight matters editorially. Recent weeks have leaned heavily into market and policy pillars; the EUSPA Demonstrators communication is the W22 funding-pillar anchor that keeps the Space Insights weekly composition balanced for Programme Manager readership.

What this means for downstream-services SMEs and Programme Managers

For SMEs operating in EO downstream services or planning to enter the market in 2027-plus, three practical reads follow.

Sector targeting matters. The 12 May EUSPA communication names insurance and finance, energy, and fisheries and aquaculture as the three sectors carried by current Copernicus Demonstrator outcomes. SMEs writing market-entry strategies should triangulate against the EUSPA-named sectors and the Copernicus data layers underneath them, not against generic EO-market projections.

Procurement and demonstration are paired. The Demonstrators communication and the Make-it-with-Space procurement framework operate as a paired institutional surface. The 19 May 2026 closing window for Make-it-with-Space is the proximate procurement vehicle; successor calls inside the Horizon Europe Cluster 4 and EUSPA's standalone procurement pipeline are the medium-term horizons.

Downstream-services revenue supports the underlying autonomy case. EUSPA's downstream-services framing reads, in Space Insights' editorial reading of the W22 mix, as a commercial layer that helps make the autonomy thesis Aschbacher framed at policy-leadership level economically legible. The EUSPA market figures — EUR 3.4 billion global EO revenue in 2023, projected to almost double to nearly EUR 6 billion by 2033, per EUSPA's 12 May framing — quantify the revenue-base trajectory inside which sustainable European space capability is being argued for at autonomy-thesis level. Sustained European downstream service markets are one of the conditions that can support durable European space capability; the Demonstrators read as evidence of that downstream layer.

What is uncertain

The EUSPA Demonstrators communication names the three demonstrators above and quantifies the aggregate EO market envelope but does not include per-demonstrator contract values or per-sector revenue breakdowns. Any sector-by-sector market-size or growth-rate figure beyond the EUSPA-published EUR 3.4 billion (2023) / nearly EUR 6 billion (2033) envelope should be sourced to additional EUSPA reporting or to independent EO market research.

The 19 May 2026 Make-it-with-Space deadline has passed at time of writing (28 May publication). The procurement outcome would normally surface through EUSPA's contract-award reporting over the following months; the timing of that publication is not pre-announced.

Forward look

Three watch items for the second half of 2026:

- EUSPA Make-it-with-Space (EUSPA-OP-07-25) award outcomes — which downstream-services consortia receive contracts under the closed 19 May window.

- Horizon Europe Cluster 4 2026-2027 downstream-services topics — successor calls to Make-it-with-Space inside the broader EU funding architecture.

- Copernicus Services 2027-plus operational continuity — EUSPA institutional positioning on Copernicus operational continuity under the EU MFF 2028 to 2034 envelope (W22 Space Insights coverage of the Aschbacher op-ed; primary path Josef Aschbacher, LinkedIn Pulse, 18 May 2026).

The EUSPA Copernicus Demonstrators publication reads as the commercial-value evidence layer for European space the autonomy week did not show. Read against the W22 mix as a whole, it is the funding-pillar anchor that grounds the policy-and-prime-architecture surfaces in actionable commercial uptake. This is a Space Insights editorial read of the week's composition, not an EUSPA statement.

Get briefings like this every Friday.

Subscribe