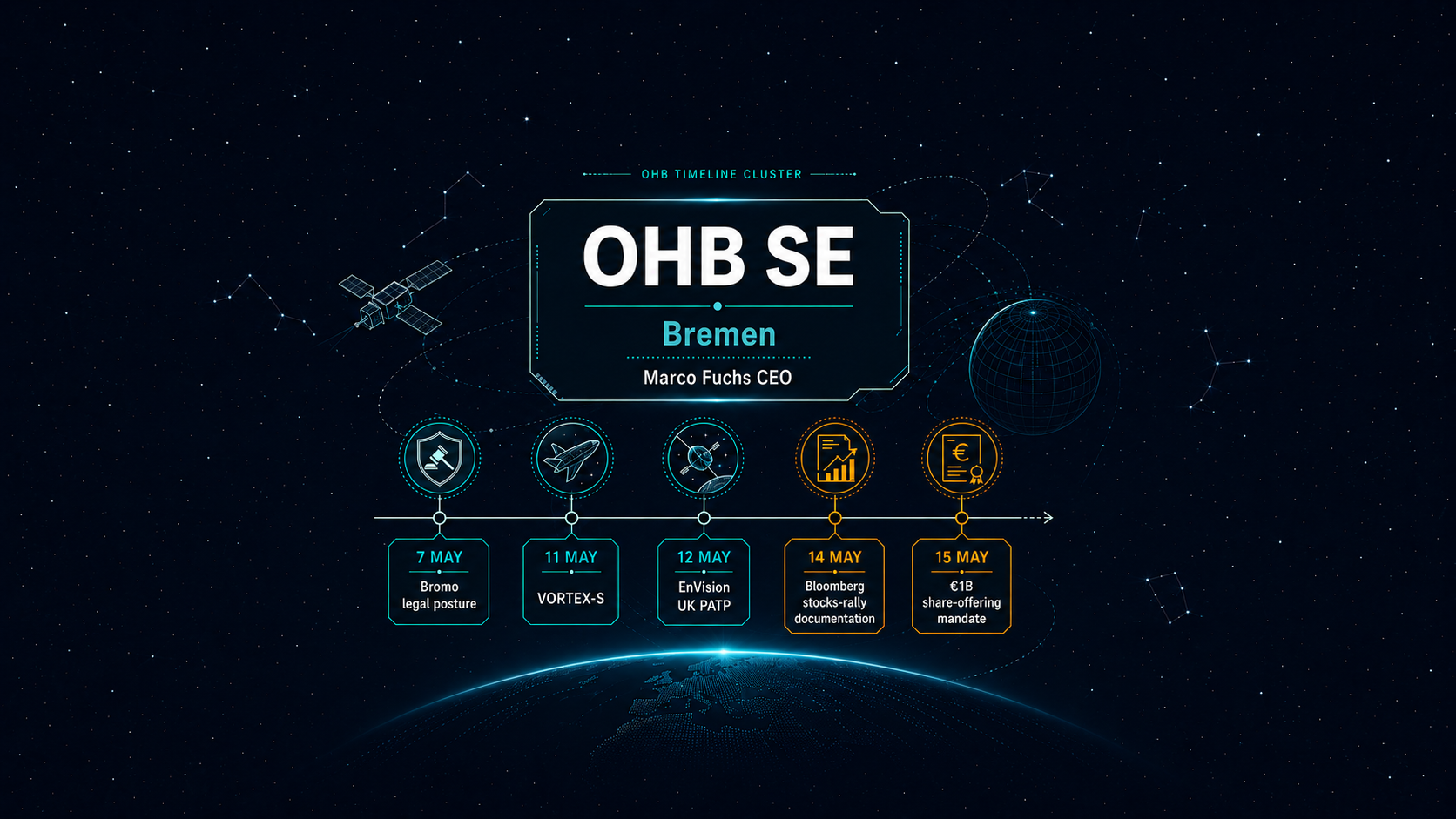

Five W21 OHB-touched signals — Bromo legal posture (7 May), VORTEX-S service-module role (11 May), EnVision UK €24M PATP (12 to 13 May), European space-stocks rally (14 May), planned share offering syndicate construction (15 May). Space Insights.

Five OHB-touched public signals landed inside ten days. On 7 May, Reuters reported OHB SE CEO Marco Fuchs saying OHB would consider legal action if EU antitrust regulators approve the Airbus-Leonardo-Thales satellite-manufacturing combination known internally as Project Bromo. On 11 May, Dassault Aviation and OHB SE announced the joint VORTEX-S spaceplane proposal to ESA, with Dassault as prime architect and global integrator and OHB as architect and integrator of the service module. On 12 to 13 May, OHB SE (12 May) and ESA's UK Member State page (13 May) announced OHB Space UK's Preliminary Authorisation to Proceed for assembly, integration and test of ESA's EnVision Venus spacecraft, contract value approximately €24 million. On 14 May, Bloomberg reported a sharp rally in European space-linked equities, including large year-on-year gains for Filtronic and OHB SE and a quadrupled Seraphim Space Investment Trust share price trading at a large premium to its last reported net asset value (figures are point-in-time and have varied across coverage). On 15 May, Bloomberg reported that OHB SE had added Berenberg and Commerzbank to a planned share offering that could raise more than €1 billion, joining Deutsche Bank, Goldman Sachs and JPMorgan on the mandate. The cluster is the read — but several elements remain conditional, reported or not yet executed.

Why the cluster reading matters

Reading the five datapoints as discrete announcements would be reasonable but incomplete. Read together, they describe a single positioning sequence. OHB SE is operating on three time horizons simultaneously: a near-term capital-markets window with the timing of the planned share offering still unconfirmed; a medium-term regulatory clock on the European Commission's competition review of the proposed Airbus-Leonardo-Thales satellite combination; and a long-term programme-delivery clock on EnVision (2031 launch) and on any ALADDIN Phase 2 award outcome.

The gatekeeper overlay for W21 flagged the OHB cluster explicitly: five OHB-touched signals plus the broader stock rally, to be consolidated into a single market-pillar narrative anchored on OHB-as-Bromo-counterparty positioning rather than presented as disconnected entries. That editorial discipline shapes this article.

The Bromo legal posture, continued

Reuters reported on 7 May that OHB SE CEO Marco Fuchs said OHB will consider legal action if EU antitrust regulators approve Project Bromo. The legal threat is not a filing; it is a public statement of intent, conditional on the Commission's eventual decision. W20 article 1 covered the institutional architecture of the statement: the Article 263 TFEU annulment route, the Phase II interested-party route, and OHB's structural position as one of the most visible independent European satellite manufacturers outside the proposed Airbus-Leonardo-Thales combination.

W21 adds context, not new substance, to the Bromo statement. The surrounding public record is now broader than it was on 7 May:

- EnVision UK PATP (€24M) — OHB Space UK is operating as a subcontractor under the EnVision mission prime, Thales Alenia Space

- VORTEX-S service-module integrator role — VORTEX-S shows a public reusable-transport architecture built around a Dassault-OHB core team, outside the proposed Airbus-Leonardo-Thales combination

- Planned share offering — Bloomberg reported a planned share offering that could raise more than €1 billion, with the mandate construction expanded on 15 May (the transaction has not yet priced)

These are not refutations of the Bromo legal threat. They add programmatic and capital-markets context to the legal posture.

The €1 billion share offering and the KKR partial exit

Bloomberg reported on 15 May that OHB SE had added Berenberg and Commerzbank to the bank syndicate for a planned share offering that could raise more than €1 billion, joining Deutsche Bank, Goldman Sachs and JPMorgan on the mandate. The transaction is described by Bloomberg as a "re-IPO" in shorthand; per the same reporting, the bank syndicate is mandated to place approximately 20 percent of KKR's OHB holdings (approximately 5.8 percent of the company) through a combination of new and existing shares designed to increase the company's free float. The Fuchs family retains around 65 percent of voting rights; KKR holds around 29 percent of the company as the principal pre-transaction minority. The transaction has not yet priced and the timing remains unconfirmed.

The W21 equity-cluster context — a broad rally in European space-listed equities, including large year-on-year gains for Filtronic and OHB SE and a quadrupled Seraphim Space Investment Trust share price at a large premium to last reported net asset value, per Bloomberg as mirrored by Yahoo Finance — is the equity-market backdrop against which any OHB transaction would be priced. The stock-rally context is relevant to the timing of any public-market transaction, but the offering has not priced and the terms remain unconfirmed.

The EnVision UK PATP and OHB Space UK's growth trajectory

Per OHB SE's primary release of 12 May, OHB Space UK signed a Preliminary Authorisation to Proceed (PATP) with mission prime contractor Thales Alenia Space for the assembly, integration and testing of ESA's EnVision Venus spacecraft. The contract value is approximately €24 million. ESA's UK Member State page, published on 13 May, confirmed the 2031 launch target and OHB Space UK's role under the prime. The subsidiary plans to grow from an initial team of around 14 employees to more than 100 highly skilled engineers over five years, alongside the build-out of a new clean-room facility at Aztec West in Bristol.

The EnVision PATP is OHB Space UK's first major contract. It gives the UK subsidiary a visible ESA mission role under Thales Alenia Space in a multi-year planetary-science programme, and a visible UK subsidiary win for a non-UK European prime in the post-Brexit European space industrial map.

The VORTEX-S service-module integrator role

Per the Dassault Aviation press kit of 11 May, Dassault Aviation and OHB SE announced a joint proposal to the European Space Agency for the VORTEX-S multipurpose spaceplane. The architecture allocates Dassault Aviation as prime architect and global integrator, and OHB SE as architect and integrator of the service module. The companies have also indicated discussions are underway with additional European space companies to expand the consortium. Per European Spaceflight coverage, the joint proposal positions Dassault and OHB to bid into ESA's restructured LEO Cargo Return Service Phase 2 call, which ESA renamed in early 2026 to ALADDIN (Autonomous LEO Accelerated Demo Docking to ISS Node) when it published the Phase 2 call on 8 January 2026 (per ESA's esa-star tender publication). Per the same European Spaceflight coverage, the Phase 2 structure runs in two slices: the first slice from October 2026 through Q4 2028 on the ISS-demonstration track, and the second slice from Q1 2029 on the commercial-LEO-destinations track. The same coverage notes that Dassault may be looking to consolidate its VORTEX-S and VORTEX-C variants into a single vehicle for the purposes of bidding on Phase 2.

The service-module role is the institutional read for OHB. Within the VORTEX-S architecture, the service module is the satellite-systems-heritage segment, drawing on OHB's existing competence base. The integrator framing — not subsystem supplier — places OHB at the architecture-decision tier rather than the subsystem-build tier. The full Phase 2 architecture and a fuller treatment of ALADDIN is covered separately in W21 Article 12.

ALADDIN is competitive and Phase 2 award decisions are pending. Whether the Dassault-OHB proposal becomes an awarded position or an architectural exercise will shape OHB's positioning in the post-Bromo European industrial map.

What is uncertain

The Commission has not published a decision on its competition review of Project Bromo at the time of writing. ESA has not announced ALADDIN Phase 2 award outcomes. OHB SE's share offering has not yet priced; Bloomberg's reporting documents the bank-mandate construction, not the transaction execution. The Reuters / U.S. News attribution of Fuchs's quote rests on wire-service primary; W20 verification flagged the underlying quotation as requiring manual eyes-on confirmation before publication and that flag carries forward. The European space-stocks rally figures (Filtronic, OHB, Seraphim) are point-in-time and have varied across coverage; the underlying Bloomberg snippets and Yahoo Finance mirror have shown different exact percentages in different reads, which is why this article presents the rally in directional terms rather than specific year-on-year percentages.

Forward look

Five watch items for the next 60 days:

- Commission competition decision or next procedural step on the Airbus-Leonardo-Thales satellite combination — clearance, conditional clearance, or further notification cycle

- ALADDIN Phase 2 process — next ESA public step on proposals, down-selection or contract awards; the Dassault-OHB VORTEX-S is among the proposals identified in this scan

- OHB SE planned share offering — pricing window not yet confirmed; the syndicate construction is the most recent public signal

- EnVision UK contract milestones — OHB Space UK's growth-trajectory delivery against the 100-plus engineer target and the Bristol clean-room build-out

- European space stocks index — the equity-cluster condition against which any OHB transaction would be priced

The reasonable read of the W21 OHB cluster is that the legal posture, the capital-markets position, the UK subsidiary growth, and the next-generation transport architecture role are converging into a single coherent counterparty stance. The institutional read is that OHB is now operating at the scale where independent positioning is a routine feature of the European space-industrial map.

Sources

- 1.Germany's OHB to consider legal action if EU clears Airbus-Thales-Leonardo satellite merger (Reuters wire — open access) — U.S. News (Reuters wire)

- 2.OHB Space UK: Growth, European Cooperation, and First Major Contract — OHB SE

- 3.UK company starts work on Envision Venus voyager — European Space Agency

- 4.Dassault Aviation and OHB team up to propose to ESA the VORTEX-S multipurpose space plane — Dassault Aviation

- 5.OHB Joins Dassault Aviation's VORTEX Spaceplane Initiative — European Spaceflight

- 6.ESA Adjusts Scope of Phase 2 of its LEO Cargo Return Services Initiative (ALADDIN renaming, 8 January 2026 call) — European Spaceflight

- 7.Autonomous LEO Accelerated Demo Docking to ISS Node (ALADDIN) — ESA tender publication — ESA (esa-star tender)

- 8.Satellite Maker OHB Said to Add Banks to €1 Billion 'Re-IPO' — Bloomberg

- 9.Space Stock Craze Comes to Europe as One British Fund Quadruples — Bloomberg (Yahoo Finance mirror)

- 10.Memorandum of Understanding to create a leading European player in space — Airbus / Leonardo / Thales

Get briefings like this every Friday.

Subscribe